Futu Research | ETF Investment Research

【High Dividend ETF】A good investment is not only a high dividend, but also growth

At the moment, global economic trends are turning, and the United States Reserve's interest rate cuts are in the market focus for consecutive months. High-dividend assets tend to be targeted for their unique income attributes during periods of decline. In a low interest rate environment, high-dividend ETFs can still provide investors with stable cash flows and relatively stable returns, making them a win-win option across the cycle.

with $Spdr Series Trust Spdr Portfolio S&P 500 High Dividend Etf(SPYD.US)$For example, the fund, which tracks the S&P High Dividend Index, aggregates a group of companies that have increased their dividends every year for more than 25 years in a row. As shown in the illustration, SPDY's share price is $SPDR S&P 500 ETF(SPY.US)$THE MAGNITUDE OF VARIATION IS BASICALLY THE SAME, AND IT IS BETTER TO SEE $iShares 20+ Year Treasury Bond ETF(TLT.US)$AND SPDY'S YIELD IS 4.59%, FAR HIGHER THAN SPY'S 1.28%.

Why do high-dividend assets have a money-making effect during a declining interest rate cycle?

First, the discount rate decreases, and the value of high-yield products increases

At the moment, the market is still focused on the expectation of a Fed rate cut on “soft ground”, that is, a moderate interest rate reduction policy to maintain steady economic growth. This soft ground is often accompanied by a broadening of monetary policy, increased market liquidity, and investors are more risk averse and willing to pursue higher downside returns. In this case, the overall valuation level of the stock market is likely to rise.

At the same time, the leveraged cash flow (DCF) model is often used in finance to assess the intrinsic value of an asset. Its essence is that future cash flows are discounted to the current value, in which the formula is “Present value = future cash flow/ (1+ discount rate) ^ time” “Discount rate = risk rate+risk premium “。 After the rate cut, the risk-free interest rate decreases, resulting in a lower discount rate in the DCF model. Reduced discount rates increase the present value of future cash flows, because the same cash flow is greater than the present value returned at a lower discount rate. Market valuations have risen as a result. This makes these assets even more of a target for money. Compared to other companies with less dividends, the extent of the increase in their valuation may be more noticeable.

Second, the spread is wider, and the income has a comparative advantage

In a cycle of falling interest rates, the most optimistic change is a risk-free fall in interest rates across the market as a whole. This means that returns on traditional, low-risk investment instruments such as bank deposits, bonds will fall synchronously. At this time, those stocks that offer stable and relatively high dividend yields will widen the gap between risk-free rates. It will be extremely attractive for investors seeking steady returns, thereby driving demand and prices for such stocks. The current dividend yield of SPYD mentioned above is approximately 4.49%, the single dividend yield is higher than the 20-year bond yield of 3.01%, and the yield is as high as 16.74% in the past year, demonstrating the strategic value of the long-term allocation.

In summary, the attractiveness of high-dividend products and the market performance of high-yield products can be boosted by rising valuations, making them an option for investors.

So, how should we choose high-dividend products?

At the heart of high dividends is the sustainability of the red, which is characterized by a sufficiently stable money-making capacity and cash flow, which requires a very good business environment. Specifically, a company with the following conditions would be a better choice:

1. The industry is relatively traditional and the way of production operations is relatively mature. According to statistics, the dividends of listed companies in each sector in 2023, coal, banking, petrochemicals, household appliances and transport are the top five industries with the highest dividend yields.

2. The business is stable, the earnings fluctuation is small and there should be some growth. The cash flow of these companies is relatively abundant, the production mode is relatively mature, the requirements for new technologies and new technologies are not up to the new industries. Therefore, the requirement for a retention ratio that can be distributed to distribute profits is not too high, and there is also the ability to implement high dividend rates. Reddish.

3. The best way to judge whether a company is happy to conduct shareholder returns is to look at its historical data. Generally speaking, a company's operational regulation is linked to making it more credible for a company to carry out a fixed annual revaluation.

4. Profit growth is crucial; when choosing a company, one should not only be attracted by high dividend rates, but also check whether the company's profit index (EPS per share) is growing year-on-year or at least stable. If a company's dividend yield is high but profits continue to slide, it is likely to foresee continued scarring in the future.

The above is a general selection of high-dividend stocks. Although everyone needs to analyze the specific issues when making investment choices, it is important to take care of multidimensional indicators such as comprehensive financial statements, historical data, and make careful investment decisions.

(Joe): Currently, the Futubull APP has a share sharing feature, and companies can use the top left corner of the page to enter the shareholder page to challenge their own high-yielding products. )

)

In addition to stocks, investing in high-dividend ETFs is also a good choice

While there are many high-dividend companies on the market that pay back to shareholders, there is a more stable and secure way to invest in stocks — high-dividend ETFs for investors who are less likely to choose stocks. It is worth noting that US-based ETFs are subject to a tax advantage for mainland investors with a 10% royalty tax, while investors in Hong Kong, Singapore and other regions incur a 30% royalty tax.

High-Dividend ETFs (also known as Dividend ETFs) are primarily used to determine the ETF's constituent stock options and the rights to decide the shareholding rights. The risks of the stocks tracked by different products can be dispersed, which is a nice product for conservative investors seeking stability.

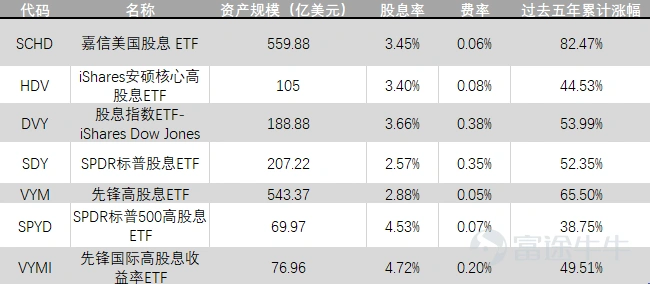

Below, we've sifted through the factors to select a few of the most mainstream high-dividend tracking ETFs on the U.S. equity market, and list their core metrics for comparison:

Based on the above table, a review of historical data, combining dividend yield and price margin. The three ETFs that have performed well over the past five years are SCHD, VYM and DVY. Below we will focus on these three products:

1. $Schwab US Dividend Equity ETF(SCHD.US)$

SCHD tracks the Dow Jones US Dividend 100 Index, which invests primarily in large equities with a history of stable dividends and comparable expected returns in the US market, with a dividend yield of 3.45%, up 82.47% over the past five years.

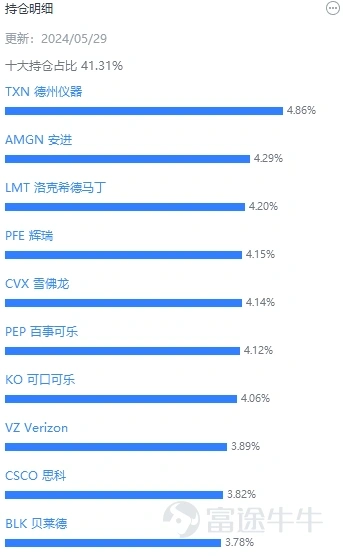

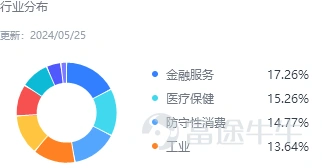

The ETF focuses on high-quality U.S. stocks that reduce the volatility of emerging markets or small-cap stocks, creating an investment portfolio made up of fundamentally strong dividend stocks. The stocks it tracks are mainly distributed in the financial services, healthcare, defensive consumer and industrial sectors, including leading companies such as Texas Instruments, Ensign, and Coca-Cola. Companies that qualify for this index often have significant competitive advantages gained through the capital and economies of scale. These companies are less affected by macroeconomic trends, stable operating conditions and positive returns to shareholders, which are expected to depreciate when interest rates fall. At the same time, for investors who prefer value investing, SCHD has a fee ratio of only 0.06%, far below the 0.48% of the ETF market average, and can benefit from CUHK with a long-term investment.

2. $Vanguard High Dividend Yield ETF(VYM.US)$

What VYM tracks is the FTSE High Dividend Yield Index, an index made up of U.S. stocks with above-average expected dividend yields. Its interest rate is 0.05% and the dividend is 2.88%, up 65.5% over the past five years.

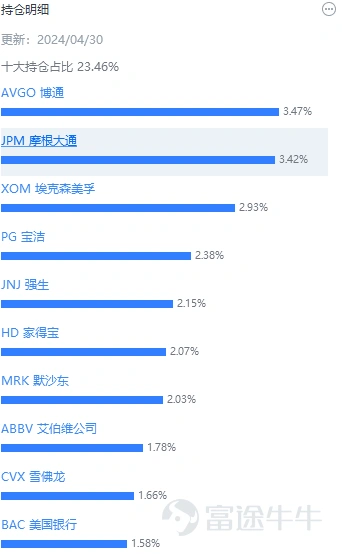

It focuses on stocks with a history of strong dividend payments, excluding real estate investment trusts and companies with uncertain dividend prospects, with a relatively high degree of diversification across sectors, including public sector companies and technology companies, and consumer defense stocks. When the market is booming, the holding of technology companies can increase their market performance so that they do not lose money, and when interest rates fall, industrial and energy holding rules can lead to stable and strong cash returns. It is worth noting that holdings of this ETF are highly dispersed, with single stocks holding no more than 3.6%, and the top ten holdings accounting for only 23.46% of supply-side holdings, and stronger defensive attributes.

3. $Ishares Select Dividend ETF(DVY.US)$

DVY tracks the Dow Jones U.S. Select Dividend Index, which contains the 100 stocks with the highest dividends on the U.S. market. It is a good choice for investors who prefer US economic stability and transparency, with a strong focus on large blue-chip stocks. Its interest rate is 0.38% and the dividend is 3.66%, up 53.99% over the past five years.

In its holdings, utilities and financial services stocks account for more than half of the weight. In a high-yield environment, the ETF performs relatively well in comparison to the market, due to the market's appetite for technology stocks. While the advantages of utilities and cycles and defensive consumer companies are evident in the forecast of falling interest rates, ETFs are also expected to perform poorly. Although its management rate is higher than the previous two, at 0.38%, it is still below the average rate level of the market ETF.

Risk Alerts

With the dual objective of pursuing stable returns and diving for capital appreciation, the US High Dividend ETF provides investors with an ideal tool to effectively spread risk and generate passive income, making it a good choice for those who seek income while willing to sacrifice some of the most capable. Nevertheless, investors should be wary of the following risks:

1. High-yield ETFs, while dispersing equity risks, still face risks from the overall market.

2. The ETF management team's decisions and actions may not be fully in the best interests of investors, and issues such as poor management quality, tracking errors, lack of transparency can lead to loss or poor performance. Investors need to pay attention to these factors to choose the right ETF and conduct effective risk management.

In addition to high dividend ETFs, in a previous tweet, we also introduced US Treasury and real estate trust funds:

Futu Research | Short-term growth rate, which can be used in many US ETFs

Futu Research | Investment Strategies for Real Estate Investment Trusts (REITs) in the Downturn

They are also quality investment products in anticipation of falling interest rates, and everyone can vote according to their preferences.